Photo from wikipedia

Variation in covariates can be used to nonparametrically identify a discrete choice model with a lagged dependent variable and discrete unobserved heterogeneity (Kasahara and Shimotsu, 2009; Browning and Carro, 2014).… Click to show full abstract

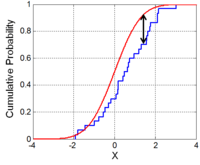

Variation in covariates can be used to nonparametrically identify a discrete choice model with a lagged dependent variable and discrete unobserved heterogeneity (Kasahara and Shimotsu, 2009; Browning and Carro, 2014). In some cases the number of support points of the unobserved heterogeneity distribution is restricted only by the number of points of support in the distribution of the covariates. This paper provides conditions under which these models can be identified with continuous heterogeneity using continuous variation in the covariates. The identification argument is related to that of Honore and Lewbel (2002) in that it requires a “special regressor” (Lewbel, 1998), but it does not assume an additively separable latent index. Identification requires only 3 time periods, neither stationarity nor time homogeneity is imposed, and the distribution of the initial condition is not restricted apart from conditions required for the special regressor. I demonstrate the result through a Monte Carlo simulation.

Journal Title: Journal of Econometrics

Year Published: 2020

Link to full text (if available)

Share on Social Media: Sign Up to like & get

recommendations!